PMFME SCHEME Complete Scheme Guide for Food Processing Entrepreneurs Bank-Ready DPRs PMFME Subsidy Support Bank Loan Assistance End-to-End Support Discuss Your Project What is the PMFME Scheme? India’s food processing sector is rapidly growing, offering huge opportunities for entrepreneurs. To support small businesses and individuals in this sector, the Government of India launched the PMFME subsidy scheme (Pradhan Mantri Formalisation of Micro Food Processing Enterprises) . This scheme is designed to help micro food processing units upgrade, expand, and become more competitive through financial assistance, training, and support. What is the PMFME Scheme? The PMFME scheme aims to formalize and strengthen micro food processing enterprises by providing financial support, skill development, and access to modern technology. It focuses on: Improving existing units Promoting new food processing businesses Encouraging value addition in agriculture Key Benefits of PMFME Scheme 1. Capital Subsidy Up to 35% subsidy on eligible project cost Maximum subsidy up to ₹10 lakh per unit 2. Support for New & Existing Units Expansion of existing food businesses Setting up new food processing units 3. Branding & Marketing Support Assistance for product branding Packaging and marketing improvements 4. Skill Development & Training Training in food processing techniques Business and quality management support Eligible Activities Under PMFME The scheme supports a wide range of food processing activities such as: Fruit and vegetable processing Spice processing Dairy products Bakery and snacks manufacturing Millet-based products Ready-to-eat and packaged foods Why Professional DPR is Important Improves loan approval chances Better rating and best interest rate Applicable fo both bank & subsidy Saves your time and effort Builds confidence with bankers Ensures lesser queries from bank Our 6 Step Process Requirement Discussion We understand your business/ idea, investment plans and funding requirements and other key points Document Collection You provide us the required documents and information. We guide you on every document needed Planning & Outlay We structure your project in funding point of view and finalize the project outlay and share with you for your feed back. DPR Preparation & Structuring We prepare the Detailed Project Report (DPR) with all requird sections, projections and annexures Review & Finalization We review the DPR with you, incorporate your feed back and finalize the details ensure the accuracy Submission & Guidance We assist in submission of bank loan documents, attend the banker query if any and guide you till the loan sanction Issues with poor DPR Loan rejection or delays Loss of time and money Poor impression with bankers Question on project viability Who Can Apply The PMFME scheme is open to: Individual entrepreneurs Self Help Groups (SHGs) Farmer Producer Organizations (FPOs) Cooperatives Micro food processing units Eligibility Criteria Applicant should be involved in food processing activities Must have basic infrastructure or plan to set up a unit Project should be viable and bankable Applicant must be willing to contribute margin money How to Apply for PMFME Scheme The application process involves multiple steps: Preparation of Detailed Project Report (DPR) Submission of application through online portal Bank appraisal and loan sanction Approval from concerned authorities Subsidy release after project implementation Why Proper DPR is Important A well-prepared DPR is critical for: Loan approval Subsidy sanction Project viability assessment Banks and authorities require: Financial projections Technical feasibility Market analysis Common Challenges Faced by Applicants Lack of proper documentation Incorrect project structuring Delay in approvals Difficulty in coordinating with banks Here’s how our team can simplify the entire journey for you We specialize in securing government benefits for your project. Our services ensure you maximize the benefit without getting bogged down in red tape: DPR Preparation: We prepare robust, bank-ready Detailed Project Reports (DPRs) that meet all the technical and financial norms of the AHIDF scheme. Document Management: We compile all necessary statutory, financial, and regulatory documents required by the lending institutions and the Department Application & Subsidy Filing: We manage the entire online application process on the portal, from initial submission to final sanction, ensuring the benifit is successfully secured for your project. Disclaimer: The information provided here is for general informational purposes only. For the most accurate and up-to-date details on the scheme, including eligibility, application process, and specific benefits, please refer to the official scheme website Ready to Start Your Project? Get expert guidance for project reports, loan and subsidies so you can focus on what you do best-Growing you business. Get Expert Consultation Need any clarification? Write to us… Find More Blogs Explore expert insights on business loans, DPR preparation, and government schemes designed to help entrepreneurs secure funding and grow with confidence. All Posts Agri Projects Bank Loan guidance MSME projects Project Reports Subsidy scheme CGTMSE Scheme Explained Read More PMEGP Subsidy Scheme Read More Mudra Loan Scheme Read More Learn More

Things to Consider Before Taking the Bank Loan

BANK LOAN GUIDE Things to Consider Before Taking a Business Loan Bank-Ready DPRs Govt Subsidy Support Bank Loan Assistance End-to-End Support Discuss Your Project Proper planning before taking a loan Taking a business loan is one of the most important financial decisions for any entrepreneur. Whether you are starting a new project, expanding an existing business, purchasing machinery, or availing benefits under government subsidy schemes, proper planning before taking a loan is extremely important. Many borrowers focus only on loan approval and overlook important aspects such as processing charges, interest calculation methods, repayment structure, and long-term financial impact. A wrong financial decision can create unnecessary pressure on the business in the future. Before applying for a project loan or business loan, it is important to understand how banks evaluate borrowers and how different loan terms can affect your finances. Below are some important points every entrepreneur should know before taking a loan. 1. Understand the Total Cost of Borrowing Most people focus only on the interest rate while comparing loans. However, the actual cost of borrowing includes several other charges such as: Processing fees Legal charges Documentation charges Valuation fees Insurance charges GST on bank charges In many project loans, processing charges alone can be significant depending on the loan amount. Therefore, always ask the bank for a complete breakup of charges before accepting the sanction. If you have a strong project profile and good financial background, you can also negotiate for lower processing fees. 2. Understand Fixed and Floating Interest Rates Before taking a loan, it is important to understand how the bank calculates interest. Fixed Interest Rate In a fixed interest loan, the interest rate remains constant throughout the loan tenure. Your EMI usually remains stable even if RBI changes interest rates. Advantages: Stable EMI Easier financial planning Disadvantages: Usually slightly higher interest rate Less benefit if market interest rates reduce later Why Professional DPR is Important Improves loan approval chances Better rating and best interest rate Applicable fo both bank & subsidy Saves your time and effort Builds confidence with bankers Ensures lesser queries from bank Our 6 Step Process Requirement Discussion We understand your business/ idea, investment plans and funding requirements and other key points Document Collection You provide us the required documents and information. We guide you on every document needed Planning & Outlay We structure your project in funding point of view and finalize the project outlay and share with you for your feed back. DPR Preparation & Structuring We prepare the Detailed Project Report (DPR) with all requird sections, projections and annexures Review & Finalization We review the DPR with you, incorporate your feed back and finalize the details ensure the accuracy Submission & Guidance We assist in submission of bank loan documents, attend the banker query if any and guide you till the loan sanction Issues with poor DPR Loan rejection or delays Loss of time and money Poor impression with bankers Question on project viability Floating Interest Rate In floating interest loans, the interest rate changes according to RBI policy rates and the bank’s benchmark lending rate. Advantages: Lower initial interest rate Benefit when interest rates reduce Disadvantages: EMI may increase if interest rates rise Long-term repayment planning becomes difficult Many business loans and project loans are sanctioned on floating interest basis. Therefore, borrowers should regularly monitor interest rate changes. 3. Understand Flat Rate vs Reducing Balance Method Many borrowers make costly mistakes because they do not understand how interest is calculated. Flat Interest Method In this method, interest is calculated on the original loan amount throughout the loan tenure, even though you continue repaying the principal every month. This can make the actual cost of borrowing much higher than it appears. Some consumer loans and vehicle loans use this method. Reducing Balance Method In this method, interest is calculated only on the outstanding loan balance after each repayment. As the principal reduces, the interest amount also reduces gradually. This method is commonly used in: Home loans Business loans Project loans Even if the interest rate looks slightly higher, reducing balance loans are often more economical in the long run compared to flat rate loans. 4. Maintain a Good Credit Score Your CIBIL score and banking history play an important role in loan approval. Banks use your credit history to evaluate: repayment discipline financial responsibility risk level A healthy credit score can help you: get faster loan approval negotiate better interest rates improve overall credibility Before applying for a loan: check your credit report clear overdue payments correct any reporting errors if present 5. Choose Between Secured and Unsecured Loans Carefully Business loans are generally categorized into: Secured Loans These loans require collateral security such as: residential property commercial property fixed deposits land Advantages: lower interest rates higher loan eligibility Unsecured Loans These loans do not require collateral but generally come with: higher interest rates stricter repayment expectations lower loan limits Choose the loan structure carefully depending on your business requirement and repayment capacity. 6. Check for Prepayment Charges Many borrowers plan to repay loans early after business income improves. However, some banks and NBFCs charge penalties for early closure or prepayment. Before signing the loan agreement, ask clearly about: prepayment charges foreclosure penalties lock-in period part-payment rules Understanding these conditions in advance can help avoid unnecessary expenses later. 7. Compare Multiple Banks Before Finalizing Do not accept the first loan offer immediately. Different banks may offer variations in: interest rates repayment tenure processing charges collateral requirements repayment flexibility If your project profile is strong and financially viable, you can negotiate better terms by comparing multiple banks and financial institutions. However, while comparing loans, do not focus only on low interest rates. Evaluate the complete loan structure carefully. 8. Prepare a Proper Project Report (DPR) A professionally prepared Detailed Project Report (DPR) significantly improves your loan proposal. A good DPR helps the bank understand: project feasibility investment structure profitability repayment capacity market potential A structured DPR generally includes: project

CGTMSE Scheme Explained

CGTMSE Scheme Explained Get Your Business Loan Up To ₹10 Crore – No Collateral Needed! Bank-Ready DPRs Govt Scheme Support Bank Loan Assistance End-to-End Support Discuss Your Project What is CGTMSE Scheme? Lets understand why this CGTMSE Scheme is absolutely a game changer for every businesses. For every aspiring entrepreneur, financing is often the biggest mountain to climb. The demand for collateral—a personal asset or property—can be a total deal-breaker for brilliant micro and small business ideas (MSMEs). But what if a government scheme was specifically designed to remove this very hurdle? Enter the Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE) scheme. This is a powerful enabler that helps you secure business loans without pledging your personal assets. It’s a safety net for the bank, which in turn means freedom for you, the borrower. The CGTMSE Lifeline: Your Collateral-Free Funding Up To ₹10 Crore The CGTMSE scheme was established by the Government of India and SIDBI to provide credit guarantee cover to banks. If your business loan defaults, CGTMSE compensates the bank for a major portion of the loss. This de-risks the loan for the bank, making them eager to fund deserving MSMEs. The headline benefit? You can now access term loans and working capital facilities of up to ₹10 Crore without pledging your residential property, factory building, or any other personal assets! A Flexible Solution: The Hybrid Security Option The scheme is designed for maximum flexibility. If your loan requirement is higher, or if the bank still requires some security, CGTMSE offers a Hybrid Security facility. This allows the bank to accept a limited amount of collateral to cover a part of the loan, while the remaining, uncovered portion is protected by the CGTMSE guarantee. It’s the perfect middle-ground for fast-growing businesses that have some assets but not enough to cover the full loan. Who & What is Covered? Beneficiaries: Any new or existing Micro and Small Enterprise (MSME) formally registered (Udyam Registration is a must) across manufacturing, services, and trading sectors. Loans Covered: Both Term Loans (for machinery, infrastructure) and Working Capital Facilities (for inventory, operations) up to the limit of ₹10 Crore. Why Professional DPR is Important Improves loan approval chances Better rating and best interest rate Applicable fo both bank & subsidy Saves your time and effort Builds confidence with bankers Ensures lesser queries from bank Our 6 Step Process Requirement Discussion We understand your business/ idea, investment plans and funding requirements and other key points Document Collection You provide us the required documents and information. We guide you on every document needed Planning & Outlay We structure your project in funding point of view and finalize the project outlay and share with you for your feed back. DPR Preparation & Structuring We prepare the Detailed Project Report (DPR) with all requird sections, projections and annexures Review & Finalization We review the DPR with you, incorporate your feed back and finalize the details ensure the accuracy Submission & Guidance We assist in submission of bank loan documents, attend the banker query if any and guide you till the loan sanction Issues with poor DPR Loan rejection or delays Loss of time and money Poor impression with bankers Question on project viability Why CGTMSE is a Game-Changer Zero Collateral Stress: Focus entirely on your business plan, not on finding security. Access to Credit: Opens formal banking channels to millions of deserving small businesses. Maximum Flexibility: The Hybrid Security feature caters to every scenario, from completely new projects to large-scale expansions. Let Us Secure Your Funding: Our CGTMSE Support The scheme is excellent, but navigating the banking and documentation process can be tedious. This is where we step in to ensure you secure the funds you need efficiently: DPR Preparation: We prepare robust, bank-ready Detailed Project Reports (DPRs) that clearly demonstrate viability, the single most important factor for a collateral-free loan. Bank Sourcing: We don’t just guide you; we help you find the suitable banks that are aggressively providing CGTMSE-backed loans in your area and sector, maximizing your chances of quick approval. Application & Liaison: We manage the entire application process, ensuring your proposal meets all the specific requirements for either the Collateral-Free or Hybrid Security route. Don’t let capital be a barrier any longer. Partner with us to leverage the power of CGTMSE and get the funding you deserve! Ready to start building your future? Disclaimer: The information provided here is for general informational purposes only. For the most accurate and up-to-date details on the scheme, including eligibility, application process, and specific benefits, please refer to the official scheme website Ready to Start Your Project? Get expert guidance for project reports, loan and subsidies so you can focus on what you do best-Growing you business. Get Expert Consultation Need any clarification? Write to us… Find More Blogs Explore expert insights on business loans, DPR preparation, and government schemes designed to help entrepreneurs secure funding and grow with confidence. All Posts Agri Projects Bank Loan guidance MSME projects Project Reports Subsidy scheme PMFME SUBSIDY SCHEME Read More PMEGP SUBSIDY SCHEME Read More MUDRA LOAN SCHEME Read More Learn More

What Are the Documents Required for a Bank Loan?

Bank Documents Guide Impotant Documents Required for a Bank Loan Bank-Ready DPRs Govt Subsidy Support Bank Loan Assistance End-to-End Support Discuss Your Project What Are the Documents Required for a Bank Loan? Securing a bank loan is one of the most important steps for starting or expanding a business. Whether you are applying for a manufacturing project, service business, MSME loan, PMEGP loan, or working capital facility, banks require proper documentation before sanctioning the loan. Many entrepreneurs feel overwhelmed when banks ask for multiple documents during the loan process. However, these requirements are a normal part of banking procedures and financial assessment. In this article, we will explain the common documents required for a business loan and why banks insist on detailed documentation before approving finance. Why Do Banks Ask for So Many Documents? Before understanding the document checklist, it is important to know why banks require these documents. Banks are lending public money and therefore must carefully evaluate: borrower credibility repayment capacity project feasibility legal compliance financial strength Proper documentation helps banks make informed lending decisions and reduce financial risk. It is not about distrust — it is part of responsible lending and regulatory compliance. Common Documents Required for Bank Loan The exact requirement may vary depending on: project type loan amount business category bank policies subsidy schemes However, below are some of the commonly required documents for business and project loans. Why Professional DPR is Important Improves loan approval chances Better rating and best interest rate Applicable fo both bank & subsidy Saves your time and effort Builds confidence with bankers Ensures lesser queries from bank Our 6 Step Process Requirement Discussion We understand your business/ idea, investment plans and funding requirements and other key points Document Collection You provide us the required documents and information. We guide you on every document needed Planning & Outlay We structure your project in funding point of view and finalize the project outlay and share with you for your feed back. DPR Preparation & Structuring We prepare the Detailed Project Report (DPR) with all requird sections, projections and annexures Review & Finalization We review the DPR with you, incorporate your feed back and finalize the details ensure the accuracy Submission & Guidance We assist in submission of bank loan documents, attend the banker query if any and guide you till the loan sanction Issues with poor DPR Loan rejection or delays Loss of time and money Poor impression with bankers Question on project viability 1. Loan Application Form The first step is submitting the official application form provided by the bank. This application usually includes: promoter details business information loan requirement project details financial information Ensure all information is filled accurately and consistently with supporting documents. 2. KYC Documents Banks require KYC (Know Your Customer) documents to verify the identity and address of the borrower. Common KYC documents include: Identity Proof Aadhaar Card PAN Card Passport Voter ID Driving License Address Proof Aadhaar Card Electricity Bill Rental Agreement Passport Utility Bills For partnership firms, companies, and LLPs, KYC documents of all directors or partners may also be required. 3. PAN Card and Income Tax Returns Income Tax Returns (ITR) help banks understand the financial background and repayment capability of the borrower. Banks may ask for: last 2 to 3 years ITR computation of income audited financial statements balance sheet and profit & loss account These documents help assess: business turnover income stability existing liabilities tax compliance 4. Bank Statements Recent bank statements are important for evaluating transaction history and financial discipline. Banks generally ask for: last 6 months to 1 year bank statements This helps assess: account conduct repayment behavior cash flow pattern existing EMI obligations Healthy banking transactions improve credibility during loan assessment. 5. Business Registration Documents Depending on your business structure, banks may ask for registration-related documents such as: MSME / Udyam Registration GST Registration Partnership Deed Company Incorporation Certificate Trade License Shops & Establishment License FSSAI License (for food businesses) Professional Tax Registration These documents establish the legal identity and operational status of the business. 6. Detailed Project Report (DPR) For project loans, one of the most important documents is the Detailed Project Report (DPR). A professionally prepared DPR helps banks understand: project feasibility investment structure profitability repayment capacity market potential A proper DPR generally includes: project cost machinery details financial projections profitability analysis break-even analysis repayment schedule working capital requirement A well-prepared DPR significantly improves the quality of the loan proposal. 7. Quotations and Cost Estimates Banks usually ask for quotations related to: machinery equipment fabrication furniture infrastructure vehicles These quotations help verify whether the project cost mentioned in the DPR is realistic and properly estimated. 8. Property Documents and Collateral Papers If the loan involves collateral security, banks may ask for: property documents sale deed tax paid receipts encumbrance certificate legal opinion valuation report Banks verify the ownership, legal status, and market value of the security property before sanctioning the loan. 9. Rental Agreement or Project Site Documents If the business operates from a rented premises, banks may require: rental agreement lease agreement NOC from property owner For owned premises: property ownership documents may be required. 10. Government Approvals and Compliance Documents Certain industries require approvals from local authorities before project implementation. Depending on the project type, banks may ask for: trade licenses pollution control NOC factory license municipal approvals plan approval fire safety approvals These approvals ensure regulatory compliance of the proposed business. Why Banks Ask for Documents in Stages Many borrowers become frustrated because banks sometimes ask for additional documents during different stages of processing. This happens because: different departments verify different aspects loan appraisal evolves gradually higher authorities may seek clarification legal and technical teams may request additional papers Therefore, document requests during processing are quite normal in project finance. Tips to Handle the Documentation Process Smoothly Ask for a Checklist in Advance Maintain Copies of All Documents Organize Documents Properly Understand Bank Limitations Be Patient During the Process Seek Professional Assistance

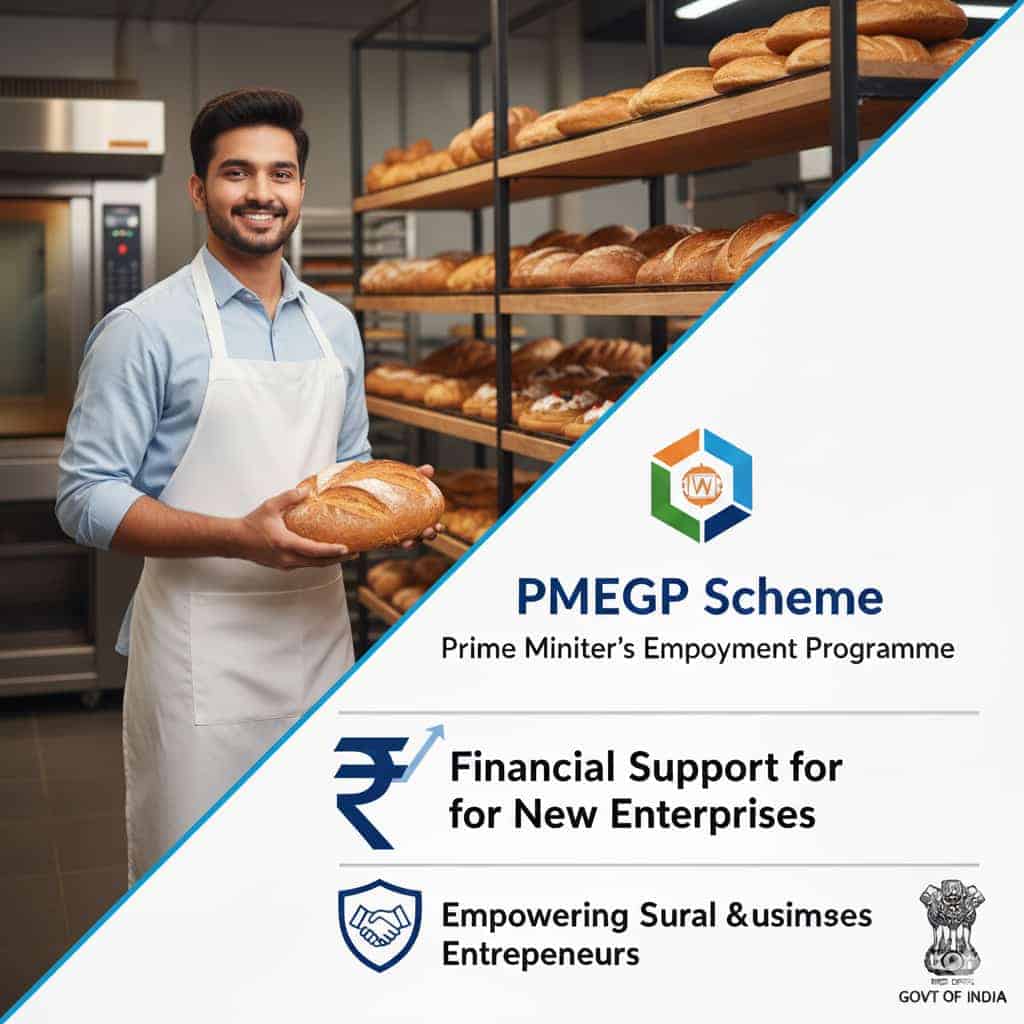

PMEGP Subsidy Scheme

PMEGP GUIDE How the PMEGP Subsidy Scheme Can Help You Start Your Business Bank-Ready DPRs PMEGP Subsidy Support Bank Loan Assistance End-to-End Support Discuss Your Project What is PMEGP Scheme? Have you ever dreamt of being your own boss, of turning a brilliant idea into a thriving business? For many aspiring entrepreneurs in India, the journey from dream to reality can seem daunting, often due to a lack of capital. But what if there was a government scheme designed to bridge that gap and provide crucial financial support? Enter the Prime Minister’s Employment Generation Programme (PMEGP) – a flagship credit-linked subsidy scheme that has been empowering countless individuals to establish micro-enterprises across the country. What is PMEGP? Launched by the Ministry of Micro, Small and Medium Enterprises (MSME), PMEGP aims to generate employment opportunities in both rural and urban areas through the establishment of new self-employment ventures, projects, and micro-enterprises. It’s a fantastic initiative that encourages entrepreneurship and helps reduce unemployment. How Does it Work? The Core of PMEGP is its Subsidy The most attractive feature of PMEGP is its significant financial assistance in the form of a subsidy. This isn’t just a loan; it’s a portion of your project cost that the government contributes, effectively reducing your financial burden and making your business idea more viable. Subsidy Structure For General Category Applicants: Rural Area: 25% of the project cost Urban Area: 15% of the project cost For Special Categories / Women: Rural Area: 35% of the project cost Urban Area: 25% of the project cost Example: If you’re a woman entrepreneur in a rural area starting a project with a cost of ₹10 lakhs, you could be eligible for a subsidy of ₹3.5 lakhs! This significantly brings down the amount you need to borrow and repay. Why Professional DPR is Important Improves loan approval chances Better rating and best interest rate Applicable fo both bank & subsidy Saves your time and effort Builds confidence with bankers Ensures lesser queries from bank Our 6 Step Process Requirement Discussion We understand your business/ idea, investment plans and funding requirements and other key points Document Collection You provide us the required documents and information. We guide you on every document needed Planning & Outlay We structure your project in funding point of view and finalize the project outlay and share with you for your feed back. DPR Preparation & Structuring We prepare the Detailed Project Report (DPR) with all requird sections, projections and annexures Review & Finalization We review the DPR with you, incorporate your feed back and finalize the details ensure the accuracy Submission & Guidance We assist in submission of bank loan documents, attend the banker query if any and guide you till the loan sanction Issues with poor DPR Loan rejection or delays Loss of time and money Poor impression with bankers Question on project viability Who Can Apply PMEGP is designed to be inclusive. Here are the general eligibility criteria: Any individual, 18 years of age or above. For projects costing above ₹10 lakhs in the manufacturing sector and above ₹5 lakhs in the business/service sector, the applicant must have at least an 8th-standard pass educational qualification. Self-help groups (SHGs) (provided that they have not availed benefits under any other scheme), institutions registered under Societies Registration Act, 1860, etc., are also eligible. What Kind of Projects are Supported? PMEGP supports a wide range of projects, primarily in the manufacturing and service sectors. From small-scale manufacturing units like bakeries or textile production to service-based businesses like repair shops, beauty salons, or IT services – if it generates employment and is viable, it likely fits the bill. How to Apply? The application process for PMEGP is streamlined and primarily online: Online Application: Visit the official PMEGP e-portal (kviconline.gov.in) and fill out the application form. Project Report: Prepare a detailed project report outlining your business idea, costs, market analysis, and financial projections. Training: Applicants are usually required to undergo an Entrepreneurship Development Program (EDP) training. Submission and Interview: Submit your application and project report to the nearest Khadi and Village Industries Commission (KVIC), Khadi and Village Industries Board (KVIB), or District Industries Centre (DIC) office. You might be called for an interview. Bank Sanction: If your application is approved by the Task Force Committee, it will be forwarded to banks for loan sanction. Here’s how our team can simplify the entire journey for you We specialize in securing government benefits for your project. Our services ensure you maximize the benefit without getting bogged down in red tape: DPR Preparation: We prepare robust, bank-ready Detailed Project Reports (DPRs) that meet all the technical and financial norms of the AHIDF scheme. Document Management: We compile all necessary statutory, financial, and regulatory documents required by the lending institutions and the Department Application & Subsidy Filing: We manage the entire online application process on the portal, from initial submission to final sanction, ensuring the benifit is successfully secured for your project. Disclaimer: The information provided here is for general informational purposes only. For the most accurate and up-to-date details on the scheme, including eligibility, application process, and specific benefits, please refer to the official website. Ready to Start Your Project? Get expert guidance for project reports, loan and subsidies so you can focus on what you do best-Growing you business. Get Expert Consultation Need any clarification? Write to us… Find More Blogs Explore expert insights on business loans, DPR preparation, and government schemes designed to help entrepreneurs secure funding and grow with confidence. All Posts Agri Projects Bank Loan guidance MSME projects Project Reports Subsidy scheme PMFME Subsidy Scheme Read More CGTMSE Scheme Explained Read More Mudra Loan Scheme Read More Learn More

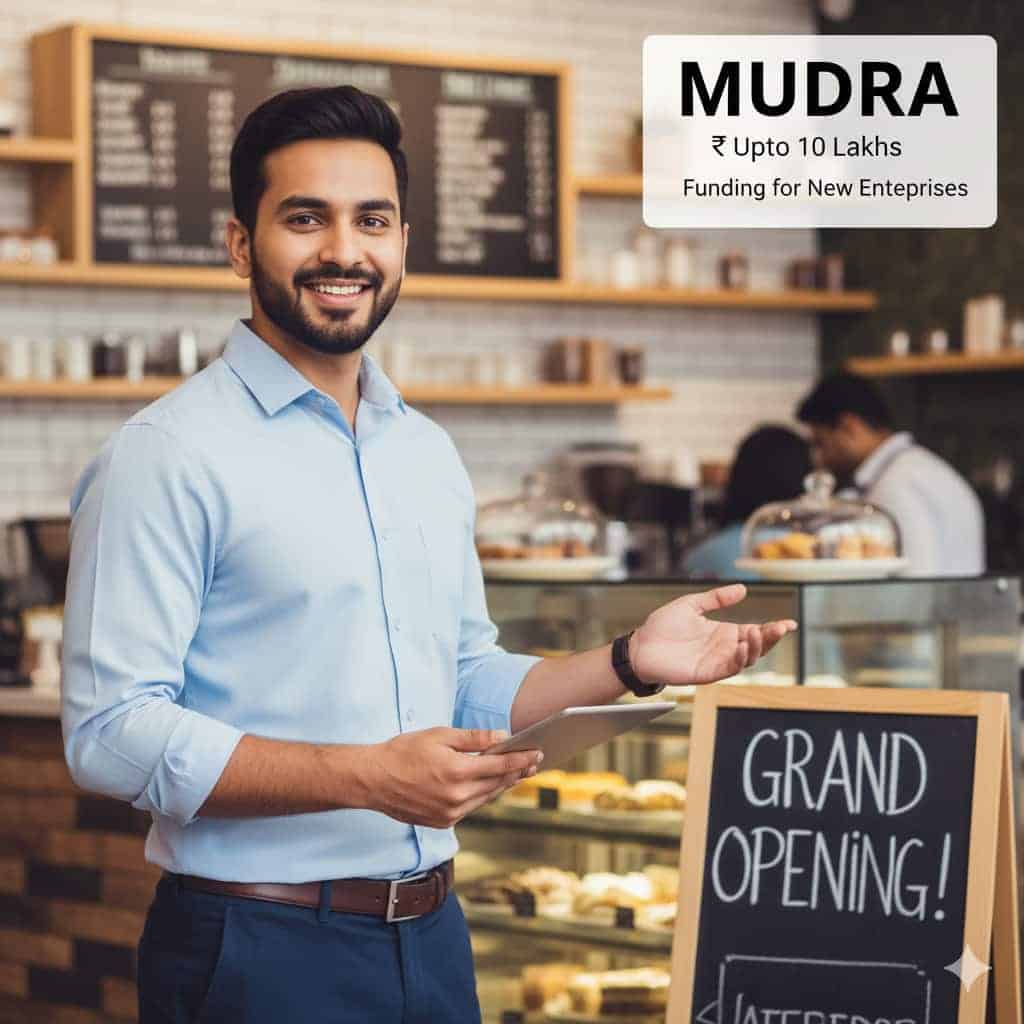

Mudra Loan Scheme

Dream Big, Start Small Your ₹10 Lakh Boost with the MUDRA Scheme Bank-Ready DPRs Mudra Scheme Support Bank Loan Assistance End-to-End Support Discuss Your Project What is Mudra Scheme? The Mudra loan scheme provides collateral-free business loans under Shishu, Kishore and Tarun categories for small and micro enterprises. Forget the confusing jargon and complicated classifications. The core message of MUDRA is simple: financial support of up to ₹10 Lakhs is available for non-farm, non-corporate micro and small enterprises. Yes, that means your small business can get the backing it needs! The Power of MUDRA: Up to ₹10 Lakhs for Your Business Growth The MUDRA scheme was launched by the Government of India with a clear mission: to “fund the unfunded.” It’s designed specifically for small businesses, street vendors, artisans, and service providers who often struggle to get loans from traditional banks because they lack collateral or a formal credit history. The biggest takeaway? You can get a loan of up to ₹10 Lakhs to start, stabilize, or grow your enterprise. This isn’t just about starting from scratch. Whether you’re a seasoned entrepreneur looking to double your inventory or a passionate individual ready to turn a hobby into a full-time venture, MUDRA is there to support a wide array of activities: Manufacturing: Setting up a small production unit, a tailoring shop, or an electronics repair store. Trading: Expanding your retail shop, becoming a distributor, or opening a new kiosk. Services: Starting a beauty parlour, a small restaurant, a transport service, or a computer repair shop. Allied Agricultural Activities The beauty of MUDRA is its simplicity and its widespread reach. These loans are disbursed through commercial banks, Regional Rural Banks (RRBs), Small Finance Banks (SFBs), Micro Financial Institutions (MFIs), and Non-Banking Financial Companies (NBFCs), making it accessible even in remote areas. Why MUDRA is a Lifeline for Small Businesses? No Collateral Required: For loans up to a certain amount (typically ₹10 Lakhs, as per the scheme’s spirit), you generally don’t need to put up collateral. This removes a massive barrier for new entrepreneurs. Affordable Interest Rates: The interest rates are usually competitive and set according to RBI guidelines, making the loans financially viable for small ventures. Flexible Repayment: Loan tenure can be flexible, allowing you to manage repayments based on your business’s cash flow. Why Professional DPR is Important Improves loan approval chances Better rating and best interest rate Applicable fo both bank & subsidy Saves your time and effort Builds confidence with bankers Ensures lesser queries from bank Our 6 Step Process Requirement Discussion We understand your business/ idea, investment plans and funding requirements and other key points Document Collection You provide us the required documents and information. We guide you on every document needed Planning & Outlay We structure your project in funding point of view and finalize the project outlay and share with you for your feed back. DPR Preparation & Structuring We prepare the Detailed Project Report (DPR) with all requird sections, projections and annexures Review & Finalization We review the DPR with you, incorporate your feed back and finalize the details ensure the accuracy Submission & Guidance We assist in submission of bank loan documents, attend the banker query if any and guide you till the loan sanction Issues with poor DPR Loan rejection or delays Loss of time and money Poor impression with bankers Question on project viability Ready to Apply? Your Next Steps Applying for a MUDRA loan is straightforward. Here’s what you generally need to do: Prepare Your Project Report: Even for a small loan, having a clear idea of what your business does, how much money you need, and how you plan to use it is crucial. Hence get the Detailed Project Report (DPR) from experts Gather Basic Documents: Typically, this includes your identity proof (Aadhaar, PAN Card), address proof, recent photographs, and relevant business licenses or registrations (if any). Approach Your Bank/Lender: Visit your nearest bank branch and inquire about MUDRA loans. They will guide you through the application process. Here’s how our team can simplify the entire journey for you We specialize in securing government benefits for your project. Our services ensure you maximize the benefit without getting bogged down in red tape: DPR Preparation: We prepare robust, bank-ready Detailed Project Reports (DPRs) that meet all the technical and financial norms of the scheme. Document Management: We compile all necessary statutory, financial, and regulatory documents required by the lending institutions Application & Subsidy Filing: We guide you through the the entire loan sanction process, from initial submission to final sanction. Disclaimer: The information provided here is for general informational purposes only. For the most accurate and up-to-date details on the scheme, including eligibility, application process, and specific benefits, please refer to the official website. Ready to Start Your Project? Get expert guidance for project reports, loan and subsidies so you can focus on what you do best-Growing you business. Get Expert Consultation Need any clarification? Write to us… Find More Blogs Explore expert insights on business loans, DPR preparation, and government schemes designed to help entrepreneurs secure funding and grow with confidence. All Posts Agri Projects Bank Loan guidance MSME projects Project Reports Subsidy scheme PMFME Subsidy Scheme Read More CGTMSE Scheme Explained Read More PMEGP Subsidy Scheme Read More Learn More

How to Get Collateral-Free Bank Loan

Complete Guide to CGTMSE Scheme Business Loans Without Collateral Security Bank-Ready DPRs Govt Subsidy Support Bank Loan Assistance End-to-End Support Discuss Your Project What is CGTMSE scheme? Many aspiring entrepreneurs and business owners face one common challenge while applying for a business loan — lack of collateral security. Banks often ask for collateral such as residential property, commercial property, land, or fixed assets before sanctioning larger business loans. However, many genuine entrepreneurs with good business ideas fail to obtain financial support because they do not have sufficient security to offer. The good news is that business loans can still be availed without collateral security under a government-backed guarantee scheme called: CGTMSE (Credit Guarantee Fund Trust for Micro and Small Enterprises) This scheme has helped thousands of small businesses and entrepreneurs obtain business loans without providing full collateral security. In this article, we will explain the CGTMSE scheme in simple terms and discuss the important factors that improve your chances of getting a collateral-free business loan. This scheme mainly supports.. CGTMSE is a Government of India credit guarantee scheme designed to support Micro and Small Enterprises (MSEs). Under this scheme, eligible business loans are covered by a government-backed guarantee. This gives confidence to banks to lend money even if the borrower does not provide sufficient collateral security. In simple words: The bank gives the business loan The government provides guarantee coverage to the bank The borrower can avail business finance without full collateral security This scheme mainly supports: manufacturing businesses service sector businesses MSMEs small business expansions new entrepreneurial ventures Loan Limit Under CGTMSE Under the CGTMSE scheme, eligible businesses can avail: Term Loan Working Capital Loan Composite Loan up to ₹10 crores, depending on project eligibility and bank assessment. However, sanction depends on: business viability repayment capacity bank comfort level project feasibility Why Professional DPR is Important Improves loan approval chances Better rating and best interest rate Applicable fo both bank & subsidy Saves your time and effort Builds confidence with bankers Ensures lesser queries from bank Our 6 Step Process Requirement Discussion We understand your business/ idea, investment plans and funding requirements and other key points Document Collection You provide us the required documents and information. We guide you on every document needed Planning & Outlay We structure your project in funding point of view and finalize the project outlay and share with you for your feed back. DPR Preparation & Structuring We prepare the Detailed Project Report (DPR) with all requird sections, projections and annexures Review & Finalization We review the DPR with you, incorporate your feed back and finalize the details ensure the accuracy Submission & Guidance We assist in submission of bank loan documents, attend the banker query if any and guide you till the loan sanction Issues with poor DPR Loan rejection or delays Loss of time and money Poor impression with bankers Question on project viability How Does CGTMSE Work? Normally, banks recover loan risk through collateral security. But under CGTMSE, the government provides guarantee coverage to the lending bank in case the loan account becomes non-performing (NPA). Depending on the category and loan structure, the guarantee coverage may go up to around: 75% 80% 85% of the outstanding loan amount. This reduces the risk for banks and encourages them to finance deserving business proposals even without strong collateral security. In return, borrowers need to pay CGTMSE guarantee fees and annual service charges as applicable. Does Every Business Loan Get CGTMSE Coverage? No. This is one of the most misunderstood aspects of the scheme. CGTMSE loan sanction is NOT automatic. The decision to provide collateral-free finance is completely based on: bank discretion project quality borrower profile repayment confidence Banks are not legally obligated to sanction loans under CGTMSE simply because the borrower requests it. The bank evaluates: project viability financial strength business experience banking history repayment capability before taking the final decision. Hybrid Security Model – Partial Collateral + CGTMSE In many cases, borrowers may have some collateral security, but it may not be sufficient to fully cover the loan amount. In such situations, banks sometimes adopt a: Hybrid / Partial Collateral Model For example: part of the loan may be covered through available collateral security remaining portion may be covered under CGTMSE guarantee This approach helps businesses avail larger loan amounts even when security coverage is partially inadequate. Factors That Improve Chances of Getting a Loan Without Collateral 1. Good CIBIL Score and Credit History Your credit history plays a major role in loan approval. Banks prefer borrowers who: repay loans on time maintain healthy banking transactions have responsible financial behavior A good CIBIL score improves: trust loan eligibility negotiation strength If you already have existing loans, ensure repayments are regular before applying for a new business loan. 2. Strong and Viable Business Model A unique, practical, and financially viable business idea always increases approval chances. Banks look for: market demand profitability sustainability repayment capability growth potential Projects with proper planning and realistic projections receive better consideration. 3. Professional Detailed Project Report (DPR) A professionally prepared DPR is one of the strongest tools while applying for a collateral-free business loan. The DPR helps the bank understand: project feasibility financial projections business model profitability repayment structure marketing strategy operational planning A strong DPR significantly improves presentation quality and creates confidence in the banker. A proper DPR generally includes: project cost machinery details income projections break-even analysis profitability statement repayment schedule working capital assessment 4. Existing Banking Relationship Existing customers with good banking track record generally have better chances under CGTMSE. If you have: long-term relationship with the bank regular account transactions existing successful loan repayment history the bank may feel more comfortable considering your proposal. 5. Expansion of Existing Business Banks are often more comfortable funding: existing businesses expansion projects proven business models Suppose your current business is already functioning well and you require additional finance for expansion. Even if your available collateral is insufficient, banks may consider partial CGTMSE coverage for the

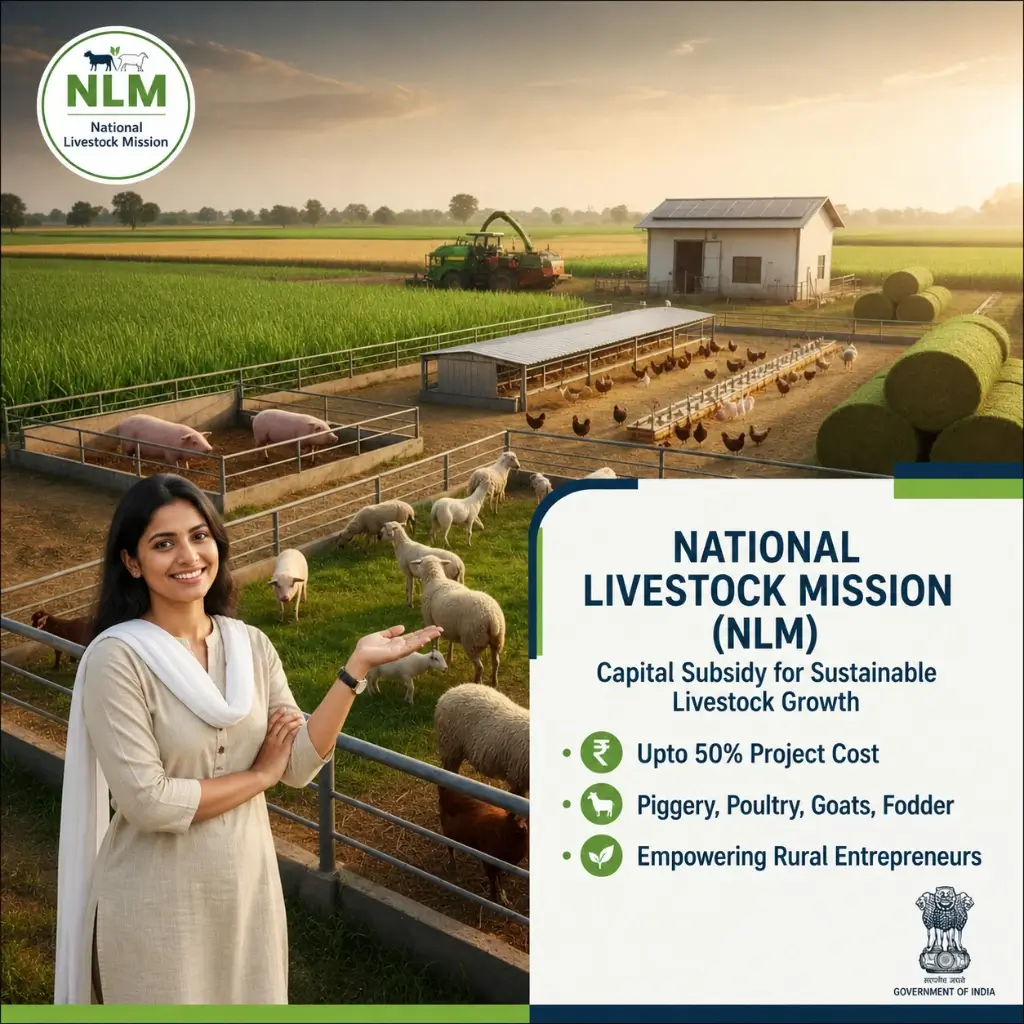

National Livestock Mission (NLM)

National Livestock Mission (NLM) Complete Guide for Poultry, Goat & Piggery Projects Bank-Ready DPRs NLM Subsidy Support Bank Loan Assistance End-to-End Support Discuss Your Project The National Livestock Mission (NLM) Scheme? The National Livestock Mission (NLM) subsidy is a key government scheme that supports poultry, goat, piggery and fodder projects with financial assistance. National Livestock Mission (NLM): India’s livestock sector isn’t just about animals; it’s about livelihoods, nutrition, and a cornerstone of our rural economy. From small farmers raising backyard poultry to entrepreneurs establishing modern sheep and goat farms, this sector holds immense potential. However, growth often requires capital for breeding, fodder, disease control, and setting up quality infrastructure. This is where the National Livestock Mission (NLM), launched by the Government of India, steps in as a powerful catalyst. The NLM is designed to promote sustainable development of the livestock sector, focusing on improving breeding, increasing fodder availability, and supporting various livestock-based enterprises. If you’re involved in sheep, goat, piggery, poultry, or fodder development, the NLM is specifically tailored to provide financial assistance and support to make your venture not just survive, but thrive. The NLM Advantage: Financial Support for Sustainable Livestock Growth The National Livestock Mission is structured to address critical gaps in the livestock sector, promoting entrepreneurship and ensuring better animal health and productivity. Unlike broad infrastructure funds, NLM directly targets specific aspects of livestock development. While the scheme has multiple sub-missions, the most impactful for entrepreneurs often revolve around: Entrepreneurship Development: Encouraging private investment in areas like sheep, goat, piggery, and poultry breeding farms. Fodder and Feed Development: Promoting scientific fodder cultivation and feed production to ensure nutritious feed for livestock. What Kind of Financial Assistance Can You Expect? NLM primarily offers capital subsidies and financial incentives for eligible projects. The exact subsidy amount can vary based on the specific component and beneficiary category, but it’s designed to significantly reduce your upfront investment. For instance, you could be looking at subsidies of up to 50% on the project cost for establishing certain breeding farms or fodder production units, with specific caps on the maximum amount. These subsidies are often released in tranches upon achieving project milestones. Why Professional DPR is Important Improves loan approval chances Better rating and best interest rate Applicable fo both bank & subsidy Saves your time and effort Builds confidence with bankers Ensures lesser queries from bank Our 6 Step Process Requirement Discussion We understand your business/ idea, investment plans and funding requirements and other key points Document Collection You provide us the required documents and information. We guide you on every document needed Planning & Outlay We structure your project in funding point of view and finalize the project outlay and share with you for your feed back. DPR Preparation & Structuring We prepare the Detailed Project Report (DPR) with all requird sections, projections and annexures Review & Finalization We review the DPR with you, incorporate your feed back and finalize the details ensure the accuracy Submission & Guidance We assist in submission of bank loan documents, attend the banker query if any and guide you till the loan sanction Issues with poor DPR Loan rejection or delays Loss of time and money Poor impression with bankers Question on project viability Key Areas of Focus Under NLM The NLM empowers a wide range of livestock-related activities: Piggery Development: Support for setting up pig breeding farms, often with substantial capital subsidies. Poultry Development: Encouraging modern poultry farms, including parent farms and hatcheries. Sheep & Goat Rearing: Financial assistance for establishing large-scale sheep and goat breeding units, promoting improved breeds. Fodder and Feed Production: Incentivizing entrepreneurs to develop fodder farms, silage making units, and feed processing plants, ensuring a steady supply of quality feed. Skill Development & Extension: Though not a direct financial incentive, NLM also supports training and knowledge dissemination to improve livestock management practices. Who Can Avail NLM Benefits? The scheme is designed to be inclusive, supporting various stakeholders: Individual Entrepreneurs: Passionate individuals looking to start or expand their livestock ventures. Farmer Producer Organizations (FPOs): Groups of farmers pooling resources to collectively improve their livestock businesses. Self-Help Groups (SHGs): Women’s groups and other community-based organizations engaged in livestock activities. Joint Liability Groups (JLGs): Informal groups collaborating for financial access. Section 8 Companies: Non-profit entities working in the livestock sector. State Livestock Development Agencies: Government bodies facilitating livestock growth. Unlock Your Livestock Potential with Our Expert Support Navigating government schemes, especially those with multiple components and specific eligibility criteria like NLM, can be daunting. From preparing detailed project reports to ensuring all documentation aligns with the scheme’s objectives, the process requires precision. Here’s how our team can simplify the entire journey for you We specialize in securing government benefits for the animal husbandry sector. Our services ensure you maximize your NLM benefit without getting bogged down in red tape: DPR Preparation: We prepare robust, bank-ready Detailed Project Reports (DPRs) that meticulously outline your project’s technical, operational, and financial viability, perfectly tailored for NLM requirements. Document Management: We compile all necessary statutory, financial, and regulatory documents required by the lending institutions and the National Livestock Mission implementing agencies. Application & Subsidy Filing: We manage the entire online application process, from initial submission to final sanction and subsequent subsidy release, ensuring you successfully avail the capital subsidy for your project. Bank & Agency Liaison: We guide you through finding suitable banks and liaise with the relevant government departments for smooth processing. The National Livestock Mission is a powerful opportunity to transform your livestock enterprise. Don’t let the complexities of the application process deter you from accessing significant financial support. Disclaimer: The information provided here is for general informational purposes only. For the most accurate and up-to-date details on the scheme, including eligibility, application process, and specific benefits, please refer to the official website. Ready to Start Your Project? Get expert guidance for project reports, loan and subsidies so you can focus on what you do best-Growing you business. Get Expert Consultation Need any clarification? Write to us…

AIF Interest Subsidy Scheme

AIF SCHEME GUIDE How the “Agriculture Infrastructure Fund” Scheme Can Transform Your Agri-Business Bank-Ready DPRs AIF Subsidy Support Bank Loan Assistance End-to-End Support Discuss Your Project What is Agriculture Infrastructure Fund (AIF)Scheme? Every year, India’s farmers produce mountains of food, yet a significant portion is lost between the field and the market due to poor handling, lack of cold storage, and inefficient logistics. This is the challenge the nation faces, and the AIF Subsidy Scheme is the government’s powerful answer. The AIF is a dedicated scheme aimed at closing this post-harvest infrastructure gap and bringing the Indian agricultural supply chain into the modern era. If you’re planning to build a warehouse, start a cold chain, or launch a tech-driven farming service, the AIF scheme offers the most attractive financial incentive available today. The Core Benefit: A 3% Interest Subsidy for 7 Years The AIF de-risks investments by providing a generous Interest Subvention (subsidy). The Financial Advantage The government commits to paying 3% of the interest on your loan every year for up to seven years. Key Rule to Remember: This subvention applies to loans up to ₹2 Crore. For projects larger than this, the subsidy is still calculated based on a maximum loan amount of ₹2 Crore. Simple Illustration of the Savings Imagine you secure a loan of ₹1 Crore from a bank at a interest rate. Standard Interest Payment: ₹10 Lakhs per year. AIF Subsidy (3%): ₹3 Lakhs per year. Your Effective Payment: ₹7 Lakhs per year. This substantial annual savings significantly reduces your operational costs in the critical start-up phase, making your project instantly more viable. What Activities Are Eligible for AIF Funding? The AIF scheme covers the entire value chain, focusing on two major areas: Post-Harvest Management Projects These focus on reducing wastage and ensuring product quality: Storage & Cold Chain: Warehouse & Silos, Cold Stores and Cold Chain, Ripening Chambers. Logistics & Processing: Logistic Facilities (Reefer Vans), Packaging Units, and Primary Processing activities (Cleaning, Milling, Drying, etc.). Quality & Waste: Assaying Units, Sorting and grading units, Farm residue/waste management infrastructures. E-Commerce: Supply chain services including e-marketing platforms Community Farming Assets & Precision Agriculture This category supports shared infrastructure and modern, sustainable technology: Technology & Automation: Purchase of Drones, Farm/Harvest Automation etc. Sustainability: Organic inputs etc. Specialized Farming: Nursery, Tissue culture, Seed Processing etc Why Professional DPR is Important Improves loan approval chances Better rating and best interest rate Applicable fo both bank & subsidy Saves your time and effort Builds confidence with bankers Ensures lesser queries from bank Our 6 Step Process Requirement Discussion We understand your business/ idea, investment plans and funding requirements and other key points Document Collection You provide us the required documents and information. We guide you on every document needed Planning & Outlay We structure your project in funding point of view and finalize the project outlay and share with you for your feed back. DPR Preparation & Structuring We prepare the Detailed Project Report (DPR) with all requird sections, projections and annexures Review & Finalization We review the DPR with you, incorporate your feed back and finalize the details ensure the accuracy Submission & Guidance We assist in submission of bank loan documents, attend the banker query if any and guide you till the loan sanction Issues with poor DPR Loan rejection or delays Loss of time and money Poor impression with bankers Question on project viability Let Us Secure Your Funding: Maximizing Your AIF Benefit The AIF scheme is a testament to the government’s commitment to modernizing agriculture, but navigating the banking, documentation, and online application process can be complex. Here’s how our team can simplify the entire journey for you: We specialize in securing government benefits for the agricultural infrastructure sector. Our services ensure you maximize the AIF benefit without getting bogged down in red tape: DPR Preparation: We prepare robust, bank-ready Detailed Project Reports (DPRs) that meet all the technical and financial norms of the AIF scheme. Document Management: We compile all necessary statutory, financial, and regulatory documents required by the lending institutions and the AIF implementing bodies. Application & Subsidy Filing: We manage the entire online application process on the AIF portal (Agri Infra Fund), from initial submission to final sanction, ensuring the 3% interest subvention is successfully secured for your project. The AIF is more than just a scheme; it’s a strategic partnership with the government to modernize and scale your business. If you have a viable plan for agricultural infrastructure, the interest subvention is the financial launchpad you’ve been waiting for. Disclaimer: The information provided here is for general informational purposes only. For the most accurate and up-to-date details on the scheme, including eligibility, application process, and specific benefits, please refer to the official website. Ready to Start Your Project? Get expert guidance for project reports, loan and subsidies so you can focus on what you do best-Growing you business. Get Expert Consultation Need any clarification? Write to us… Find More Blogs Explore expert insights on business loans, DPR preparation, and government schemes designed to help entrepreneurs secure funding and grow with confidence. All Posts Agri Projects Bank Loan guidance MSME projects Project Reports Subsidy scheme PMFME Subsidy Scheme Read More National Livestock Mission (NLM) Read More AHIDF Interest Subsidy Scheme Read More Learn More

How to Improve Your Chances of Getting Business Loan

BANK LOAN GUIDE How to Improve Your Chances of Getting a Business Loan Bank-Ready DPRs Govt Subsidy Support Bank Loan Assistance End-to-End Support Discuss Your Project Turning business ideas into reality Starting a business or expanding an existing project requires proper financial planning. Most commercial projects involve significant investment in infrastructure, machinery, working capital, and operations. Since arranging the complete investment personally is difficult for most entrepreneurs, bank loans play an important role in turning business ideas into reality. Today, many government schemes such as PMEGP, Mudra Loan, Stand-Up India, and PMFME are also linked with bank finance. This means proper project planning and loan approval have become essential for entrepreneurs looking to avail subsidy benefits and financial support. However, getting a business loan is not just about submitting an application form. Banks evaluate the promoter, project viability, repayment capacity, documentation, and financial planning before sanctioning the loan. Understanding this process can significantly improve your chances of approval. Below are some practical points every entrepreneur should know before approaching a bank for a project loan. 1. Understand Your Project Clearly Before visiting a bank, you should have proper clarity about your proposed business. Bankers expect the promoter to understand: Nature of the business Total project cost Machinery and infrastructure requirements Working capital needs Expected income and profitability Market demand for the product or service If you are unable to explain your project properly, it creates doubt about your seriousness and preparedness. A confident and informed promoter always creates a better impression. 2. Prepare a Professional DPR (Detailed Project Report) One of the most important documents for business loan approval is the Detailed Project Report (DPR). A professionally prepared DPR helps the bank understand the project clearly and evaluate its feasibility. A good DPR generally includes: Business overview Project cost estimation Machinery details Financial projections Profitability analysis Repayment schedule Market analysis Working capital assessment Submitting a structured DPR before the bank asks for it creates a positive impression and shows that the promoter has done proper planning. Why Professional DPR is Important Improves loan approval chances Better rating and best interest rate Applicable fo both bank & subsidy Saves your time and effort Builds confidence with bankers Ensures lesser queries from bank Our 6 Step Process Requirement Discussion We understand your business/ idea, investment plans and funding requirements and other key points Document Collection You provide us the required documents and information. We guide you on every document needed Planning & Outlay We structure your project in funding point of view and finalize the project outlay and share with you for your feed back. DPR Preparation & Structuring We prepare the Detailed Project Report (DPR) with all requird sections, projections and annexures Review & Finalization We review the DPR with you, incorporate your feed back and finalize the details ensure the accuracy Submission & Guidance We assist in submission of bank loan documents, attend the banker query if any and guide you till the loan sanction Issues with poor DPR Loan rejection or delays Loss of time and money Poor impression with bankers Question on project viability 3. Arrange Proper Quotations and Cost Estimates Banks often verify whether the project cost mentioned in the DPR is realistic. Therefore, it is advisable to collect quotations from machinery suppliers, equipment vendors, fabricators, or service providers related to your project. For example: Manufacturing units can collect machinery quotations Food processing units can collect processing equipment estimates Agricultural projects can collect greenhouse or irrigation quotations This improves the credibility of your proposal and supports the project cost calculations. 4. Explain Your Marketing Plan Many business projects fail not because of production problems, but because of poor marketing. Therefore, bankers are keen to know how you plan to sell your products or services. You should be prepared to explain: Target market Customer segment Distribution plan Existing business contacts Tie-ups or supply arrangements Online or offline sales strategy Even a simple but practical marketing approach can improve confidence in your project. 5. Maintain Transparency with the Bank Never hide existing loans, financial liabilities, or repayment history from the bank. Banks can verify loan information through your CIBIL report and banking records. If you have faced repayment issues in the past, explain the genuine reasons honestly. Transparency creates trust, while concealment creates suspicion. Similarly, avoid discussing unrelated personal financial problems during project discussions. The bank wants confidence that the loan amount will be used properly for the proposed business. 6. Maintain Good Banking and CIBIL History Your banking behavior plays an important role in loan approval. Timely repayment of existing loans, proper account maintenance, and a healthy CIBIL score improve your credibility. A strong financial track record signals that you are financially disciplined and capable of handling business finance responsibly. Even if your CIBIL score is slightly lower, a properly structured project with genuine explanation and supporting documents can still improve your chances. 7. Be Ready to Invest Promoter Contribution Many first-time entrepreneurs expect banks to finance 100% of the project cost. In reality, banks expect the promoter to invest a certain portion of the project from their own side. This is known as the promoter’s contribution or margin money. Promoter contribution shows: seriousness towards the project financial commitment willingness to share project risk Projects where the promoter invests their own funds generally receive better confidence from banks. How BankOn Can Help You At BankOn, we assist entrepreneurs and businesses with professional project planning and loan documentation support. Our services include: Detailed Project Report (DPR) Preparation CMA Data Preparation Applicable subsidy Assistance Bank Loan Documentation Support Financial Projection Preparation We prepare customized bank-ready DPRs based on your project type, bank requirement, and financial structure. Conclusion Getting a business loan is not only about documentation — it is about presenting a practical, well-planned, and financially viable project to the bank. A sincere promoter with proper planning, transparent financials, realistic projections, and professional documentation always stands a better chance of obtaining loan approval. If you are planning to start